Britain Is No Longer Governed. It Is Brokered.

PFI was only the prototype. Britain has learned to turn hospitals, bills, children's homes, data platforms and public contracts into private income streams backed by compulsion, regulation and the impossibility of walking away.

Britain retains every public duty but outsources every means of fulfilling them. The result is not privatisation, not socialism, not a free market. It is rentier government: private income manufactured from public compulsion, brokered by a state too hollow to build and too frightened to be honest.

Privatisation is too blunt a word for what now happens. It implies the state sells something and retreats. But the modern British state rarely retreats. It keeps the legal duties, keeps the regulation, keeps the guarantee, keeps the political promise, keeps the monopoly on compulsion. Then it invites private actors to finance, operate, interpret, house, code, advise and maintain the systems on which those duties depend.

What remains is not a market. The public cannot opt out of water, electricity, healthcare, child protection, courts, roads, tax systems, policing, waste collection, planning, public records or state databases.

Nor is it public ownership. The state does not own enough, build enough, know enough, retain enough or control enough to call it sovereignty. It brokers. It turns necessity into revenue, compulsion into cashflow, statutory obligation into seller power, and institutional weakness into private yield.

This is a broker state.

It does not appear all at once. It arrives in fragments: a hospital deal here, a regulated asset there, a software contract somewhere else, a placement market in one corner, a procurement framework across the whole shop. Each decision looks local and reasonable. Nobody announces a system. But a system is precisely what emerges, and after three decades, the structure is visible to anyone willing to trace the wiring.

Public Need Has Become an Asset Class

Across infrastructure, utilities, social care, digital platforms and government procurement, the same architecture recurs. The state identifies a public need. It lacks the money, the delivery capacity, or the political nerve to meet it directly. So it constructs an arrangement: private capital finances, builds or operates the asset; the public pays through taxes, bills, regulated charges, council budgets or future obligations; and the state sits between them, brokering the deal, absorbing the political risk, and calling the result "partnership."

The vocabulary shifts with each generation. PFI becomes PF2 becomes PPP becomes "investment model" becomes "delivery vehicle" becomes "regulated asset base" becomes "strategic supplier" becomes "transformation partner." The words get softer as the obligations get harder.

What does not change is the underlying transaction. The state supplies the compulsion. The market supplies the invoice.

The Public Accounts Committee found in July 2025 the Treasury's focus on keeping investment off the government's balance sheet had been a key driver of private financing decisions under PFI, giving the illusion of lower public borrowing while detracting from value for money. The same committee noted the Treasury has yet to identify which financing models represent value for money.

The model was not discredited and replaced. It was discredited and relabelled.

What A Broker State Looks Like

A definition is needed, because the term "privatisation" no longer covers what is happening, and the term "public-private partnership" was designed to prevent anyone from understanding it.

The broker state is what emerges when government retains the legal duties, political promises and coercive powers of the public realm, but relies on private actors to finance, deliver, operate, interpret and maintain the systems on which those duties depend.

| What the state retains | What private actors receive | What the public gets |

|---|---|---|

| Legal compulsion | Long-term contracts | Bills |

| Statutory duties | Regulated returns | Charges |

| Regulation | Placement fees | Taxes |

| Planning power | Management fees | Poorer services |

| Taxation power | Consultancy income | Future liabilities |

| Bill-payer compulsion | Software dependency | Waiting lists |

| Public guarantees | Infrastructure yield | Opaque accountability |

| Citizen data | Government-backed demand | Reduced sovereignty |

| Monopoly demand | Exit value | No meaningful opt-out |

| Moral legitimacy | Risk protection | Rescue costs |

The minister announces. The quango approves. The supplier bills. The citizen pays.

How The Machine Works

The broker state does not operate through a single mechanism. It operates through six, each reinforcing the others. Separately, each looks like an administrative choice. Together, they constitute a regime.

Acronym Renewal Is The First Defence

Bad models do not disappear. They are renamed. PFI was abolished as a brand in 2018. PF2 was scrapped alongside it. But the 10-Year Infrastructure Strategy published in 2025 explicitly discusses new public-private partnership models for infrastructure, while carefully insisting these are not PFI.

The NAO published a lessons-learned report on private finance for infrastructure in March 2025 precisely because government is again considering private finance models, drawing on over 140 past NAO publications to set out guidance.

The ICAEW, in evidence to the Public Accounts Committee, recommended the government should not adopt the PFI approach of seeking off-balance-sheet treatment, noting the hurdles necessary to achieve such accounting classification make it difficult to allocate risk appropriately and report an honest balance sheet to Parliament.

The most important trick in British government is not policy innovation. It is acronym renewal. Call the same transaction by a different name, and a generation of scrutiny evaporates.

Displacement Hides The Cost

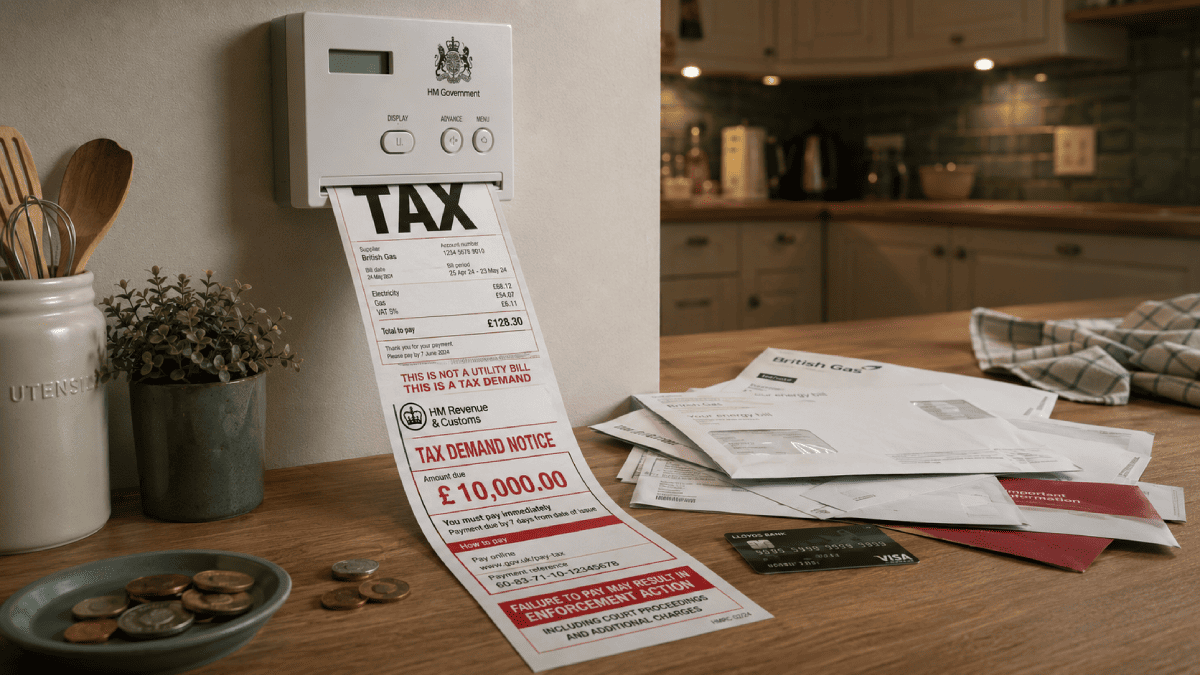

The cost does not vanish. It moves. From tax to bills. From borrowing to contracts. From the national balance sheet to council distress. From capital spending to household standing charges. From government liability to regulated consumer charges. From visible debt to invisible future payments.

The Regulated Asset Base model, now used or proposed for projects including Sizewell C and the Thames Tideway Tunnel, is the cleanest example. Instead of the government borrowing to build a power station and accounting for it on the public books, the cost is routed through consumer bills. Investors receive a guaranteed return over the asset's lifetime. The Treasury gets distance. Investors get certainty. The public gets a monthly direct debit.

A displaced cost is still a cost. It has simply been relocated to somewhere voters cannot easily find it.

The modern state does not always cut spending. It launders it.

Captivity Guarantees The Revenue

The model works best where people cannot walk away. You cannot opt out of water. You cannot opt out of electricity. You cannot refuse healthcare for your child, decline the court system, avoid the road network, unsubscribe from the tax authority, or delete yourself from the national database. These are not markets. They are compulsions. And compulsion is the most bankable asset in infrastructure finance.

The safest customer is the one who has no choice.

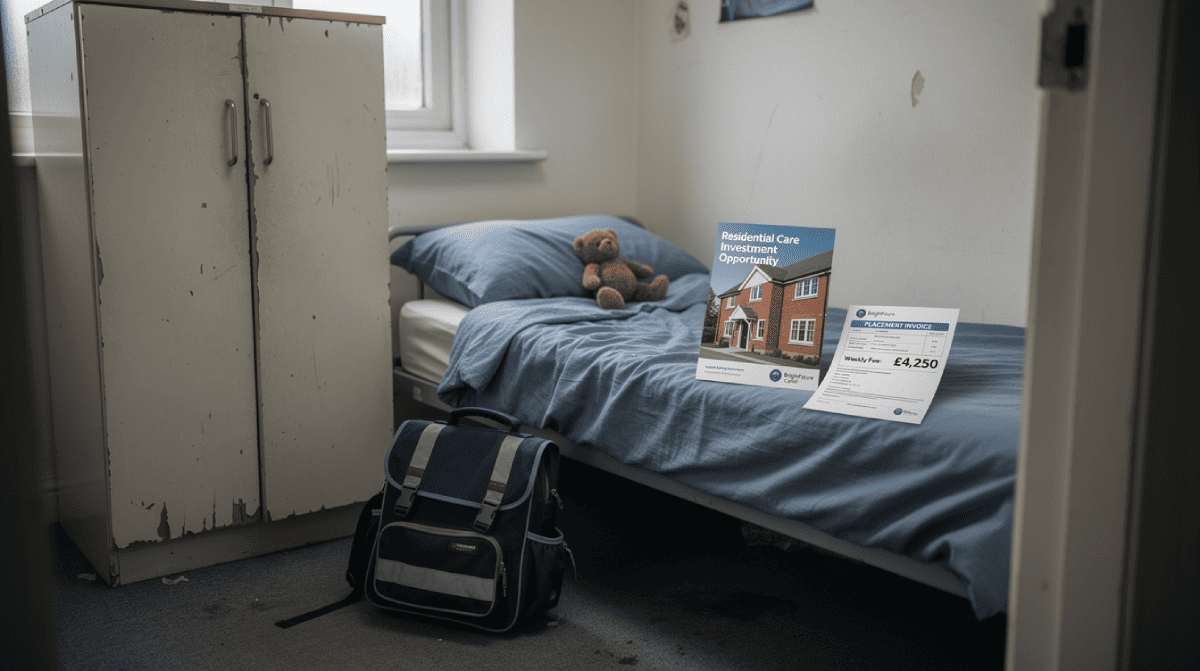

Children's residential care is the starkest moral proof. Councils carry a statutory duty to place vulnerable children. Private providers dominate provision. A desperate local authority buying an emergency placement for a child in crisis is not a consumer exercising choice. It is a distressed purchaser under legal obligation. The pricing reflects the desperation, not the value. The PAC noted in its 2025 report the significant scale of privately financed infrastructure, including around £9 billion invested through Regulated Asset Base models alone, with the government recently committing £14.2 billion to Sizewell C.

Across every sector, the same feature appears: the revenue stream is underwritten not by customer satisfaction but by the impossibility of refusal.

Public Authority Converted Into Private Guarantee

In the textbooks, private finance earns its higher cost by absorbing risk. In practice, much of the risk stays with the public. The state absorbs political risk, planning risk, demand risk, regulatory risk, rescue risk, continuity risk and reputational risk. Private actors receive contracted revenue, regulated returns, public guarantees, protected tariffs and emergency demand.

The PAC heard evidence of a "misplaced belief" among public bodies transferring risk to the private sector equated to managing it, producing "false assurance that the problem lies elsewhere."

When Carillion collapsed in 2018, the government had to keep schools, hospitals and prisons running because statutory services do not stop when a contractor goes bankrupt.

The risk had been "transferred" on paper. It returned through the front door in practice.

The state cannot outsource the duty. It can only outsource the invoice. And when the invoice becomes unpayable, the duty comes home.

In theory, the risk is priced. In practice, the public service still has to exist tomorrow morning.

Dependency Is The Product

The longer a private arrangement lasts, the harder it becomes to leave. Dependency accumulates through contract complexity, proprietary technology, data architecture, staff knowledge, supplier relationships, maintenance systems, legal exposure and sheer institutional inertia. A vendor becomes powerful not because its product is irreplaceable, but because replacing it becomes more frightening than tolerating it.

This is why Parliament's Science, Innovation and Technology Committee called Palantir's expanding presence across the UK public sector an "unacceptable point of weakness."

It is why the government is now reviewing the £330 million, seven-year NHS data platform contract ahead of its 2027 break clause, examining trust, confidentiality and reliance on a single US supplier.

And it is why the same pattern repeats with cloud providers, consultancies, outsourcers and systems integrators across Whitehall.

The old PFI trapped the state inside a building for 30 years. The new version traps the state inside someone else's operating system. The timeframes are shorter. The lock-in can be deeper.

A vendor becomes entrenched when replacing it costs more politically, technically and financially than renewing. At which point the contract ceases to be a contract. It becomes a dependency.

Moral Laundering Wraps Every Deal In Necessity

Every arrangement arrives wrapped in urgent need. We need hospitals. We need clean energy. We need children's homes. We need data modernisation. We need affordable housing. We need infrastructure. We need delivery partners. We need consultants. We need emergency accommodation. We need resilience. We need net zero. We need growth.

And often the need is real. Often it is desperate. Often there is no short-term alternative.

The need is real. The structure is the scandal.

The trick is not to invent fake needs. It is to use genuine needs to justify arrangements whose costs, dependencies, and distributional consequences nobody examines until decades later, when the contracts are signed, the capacity is lost, the suppliers are embedded and the minister who brokered the deal has long since left office.

This Is Not Free-Market Capitalism

The distinction matters, because defenders of these arrangements invariably retreat to the language of the market. Private enterprise. Competition. Efficiency. Risk. Choice.

- In a functioning market, the customer can walk away. In most of these arrangements, the customer is legally compelled to pay.

- In a functioning market, suppliers face the risk of failure. In most of these arrangements, the state is the rescuer of last resort, because the public service must continue regardless of who holds the contract.

- In a functioning market, prices are set by competition. In regulated asset base models, placement markets, software monopolies and framework agreements, prices are set by regulation, scarcity, dependency or statutory obligation.

The customer cannot walk away. The state cannot let the service fail. The supplier knows both of these things.

This is not capitalism, because capitalism involves risk. It is not socialism, because socialism involves ownership. It is not even ordinary privatisation, because the state has not simply stepped back. It has stepped sideways, using law, regulation, contracts and public compulsion to manufacture private income streams from things citizens cannot avoid.

It is rentier government: private return generated by public necessity.

This Is Not A Serious State

A serious state does not avoid cost by hiding it. It does not outsource capacity until it cannot govern what remains. It does not confuse procurement with policy. It does not treat a supplier framework as a substitute for institutional knowledge. And it does not call everything "partnership" to obscure the fact it no longer has the muscles to do the work itself.

The PAC found the UK's uncertain infrastructure environment has weakened the specialist skills essential for successful project delivery, with contracting authorities often lacking in-house expertise to make critical decisions on complex projects, placing the public sector at a persistent disadvantage.

Gross public-sector procurement spending reached £434 billion in 2024/25, a rise of £19 billion on the previous year. Of the £249 billion spent on procurement excluding capital in 2024/25, ten per cent went directly to just 39 firms designated as "Strategic Suppliers" by the Cabinet Office.

A state spending nearly half a trillion pounds a year on procurement while simultaneously lacking the specialist skills to manage it is not a state partnering with the private sector. It is a state being administered by it.

A weak state brokers what a serious state would build, own, regulate honestly or refuse to promise.

The Public Pays Three Times

Every failed model has a bill. The broker state sends it three times. The public pays as customer, as citizen and as guarantor.

As taxpayer, bill-payer, and customer

Through taxes, utility bills, council tax, service charges, standing charges, placement fees, regulated tariffs and future obligations extending into the 2050s. Public bodies are due to pay £136 billion in unitary charges on the 665 remaining PFI contracts alone, with half of these contracts expiring within the next decade. This is money owed on deals already signed, for assets already built, many of which are deteriorating.

Through worse services

Through longer waiting lists, crumbling school buildings, children in illegal placements, delayed infrastructure, lost data sovereignty, and institutional knowledge walking out of the door every time a contract changes hands. The broker state does not merely cost more. It delivers less, because the incentive structures reward financial engineering, not outcomes.

As guarantor of last resort

When the model fails, the public pays again, because essential services cannot simply collapse. Carillion demonstrated this in 2018. Every failing care home, every expiring PFI contract with a deteriorating asset, every software platform too embedded to replace, every outsourcer too integrated to remove, presents the same grim arithmetic: the state must rescue what it paid someone else to run.

Other People's Money Corp, PLC

The question is no longer whether Britain should use the private sector. Of course it should, where it adds value, where competition is genuine, where risk is honestly priced and where exit is possible without service collapse. The question is whether the state remains sovereign over the systems it promises to provide.

A serious government would ask, before every major arrangement:

- Is this cheaper over the full life of the asset, or only cheaper on today's balance sheet?

- Can the public body exit without service collapse?

- Is demand genuinely competitive or captive?

- Is risk actually transferred, or merely repriced?

- Does the state retain enough internal knowledge to govern the contract?

- Are bills being used to disguise taxation?

- Are vulnerable people being converted into revenue streams?

- Does private finance create value, or merely disguise borrowing?

- Who owns the data model, the workflow, the intellectual architecture?

- Is there a public, mutual or non-profit fallback?

- Would ministers still defend the model if its costs appeared as tax?

These are not radical questions. They are basic due diligence. The fact they are rarely asked before major commitments, and only investigated by select committees years afterwards, tells you everything about the institutional culture producing these deals.

The PAC concluded the Treasury has no comprehensive evaluation record and has never determined the overall costs and benefits of its financing models, even while planning the next generation of privately financed projects.

A country preparing to spend over a trillion pounds on infrastructure without having evaluated whether its financing models deliver value for money is not making policy. It is making bets with other people's money and other people's futures.

The Officials Carry The Rentier Disease

Rebranding ensures the model survives every scandal. Displacement ensures the cost is never visible in the right place. Captivity ensures the revenue stream is guaranteed. De-risking ensures private returns are protected while public liability is unlimited. Dependency ensures the state cannot exit. And moral laundering ensures every arrangement sounds like compassion, modernisation, or growth.

Together, they produce a state with all the obligations of public service and none of the capacity; a private sector with all the revenue of public provision and little of the risk; and a public bearing costs it was never honestly told about, receiving services it cannot escape, and underwriting failures it never authorised.

The new rentier state does not need to own the public realm; only to collect from it. It does not need to abolish democracy; only to relocate decisions into contracts, bills, regulators, frameworks and technical systems where accountability becomes too fragmented to grasp and too complex to explain at a town hall meeting.

PFI was not the mistake Britain learned from.

It was the prototype.

The infrastructure pipeline, the regulated asset base, the placement market, the data platform, the strategic supplier, the transformation partner, the framework agreement: these are the successors. Different surfaces. Same underlying architecture. Public need, converted into private income, brokered by a state too hollowed out to do the work itself and too frightened to tell the public what it really costs.

Britain does not lack money, enterprise or ingenuity. It lacks a governing class willing to borrow honestly, build directly, own strategically, pay visibly, and tell voters the truth about the price of civilisation.

Until it finds one, the broker state will keep doing what it does best: arranging the country's needs into someone else's yield, one contract, bill, placement, platform and framework at a time.