The Commonwealth Society Framework: Replacing State Pensions With True Security

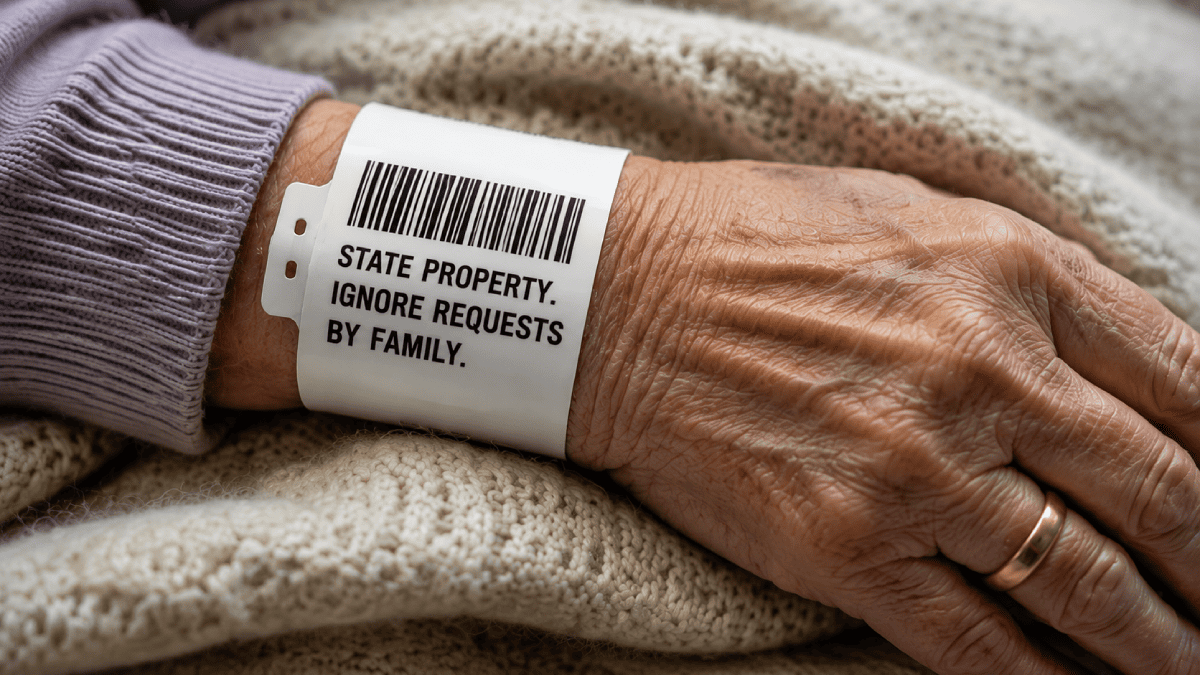

The state hands the old a weekly cheque and calls it kindness. It buys just enough to survive alone in a quiet house, then leaves the funeral and the probate to your children. There is a larger answer: owned capital, mutual societies you vest into for years, and an old age among people who know you.

Britain did not stumble into a pension crisis because a minister forgot to adjust a formula. The crisis was built into the design. Workers were told they were paying into something. They were paying for something instead, and the gap between those two prepositions is the whole story.

National Insurance was sold as a savings tin with your name on it. In practice the money went out again the same week it arrived, spent on whichever pensioners, patients and claimants happened to be alive at the time. Nothing was set aside. No fund grew quietly in your honour.

When your turn came, the bargain depended entirely on enough younger people existing beneath you to pay your claim, exactly as you had once paid theirs.

It worked beautifully for as long as Britain kept producing children. Then it stopped producing them.

And the thing itself is not a payment. This is the point to grasp before any of the mechanics: the failure of the state pension is not first a failure of money but a failure of life. A larger cheque does not answer the questions which actually frighten people about growing old, which are about loneliness, widowhood, decline, care and the chaos left behind at death. The replacement is not a better cheque. It is an institution, and the financial machinery exists only to feed it.

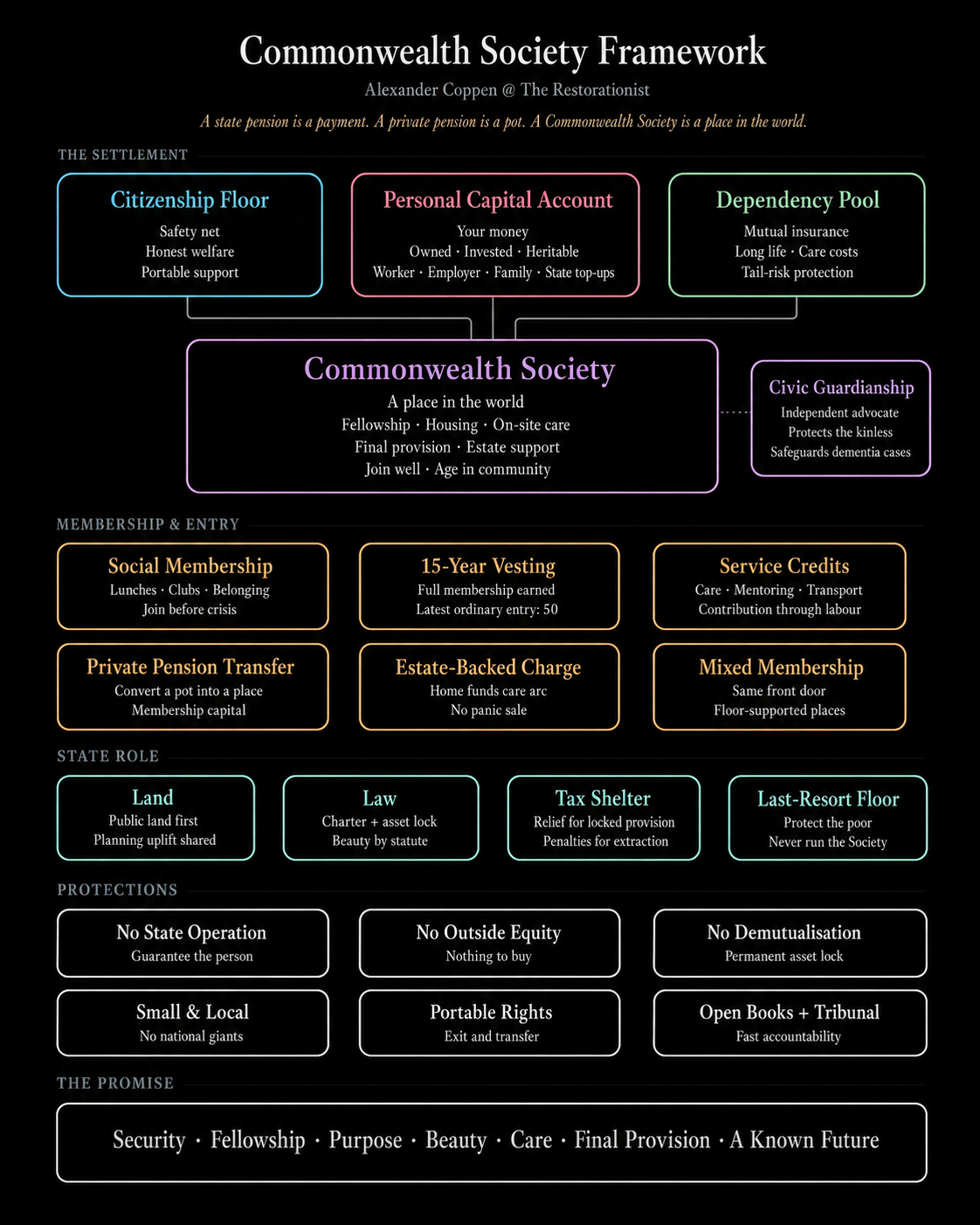

A state pension is a payment. A private pension is a pot. A Commonwealth Society is a place in the world, and the place is the settlement.

The Commonwealth Framework In Brief

For readers who want the overview before the detail, the whole proposal reduces to four parts and a handful of rules.

- The Citizenship Floor. An honest, tax-funded poverty net for anyone who reaches later life without enough to live on. Welfare, openly named as welfare, and portable: it can pay a person's way into a Society or cover ordinary living costs where there is none nearby.

- The Personal Capital Account. Real, owned, invested money built over a working life from contributions that already leave your pay packet today, gathered into one account with your name on it. It makes "I paid in" true at last, and whatever is left passes to your family.

- The Dependency Pool. Mutual insurance against the two risks no savings pot can carry alone: needing years of care, and living far longer than your money was meant to last.

- The Commonwealth Society. A small, beautiful, member-owned institution you join while still well, contribute to for years, and age into among people who know your name. It provides housing, fellowship, on-site care, the handling of death, and help for the family through grief and probate. This is the settlement. The other three feed it.

- The state's role is hard-limited. It supplies land, law, tax shelter and the last-resort floor. It never runs a Society.

- The protections are hard. Asset-locked so it cannot be sold or demutualised, capped in size so it stays local, walled internally so no one body owns your whole life, and guarded for the demented and the kinless by independent advocates.

Everything below is an expansion of those points, the worked life of a real member, and the answer to the obvious questions: who can start one, who pays for what, and what stops it being captured.

Why The Old Machine Cannot Be Saved

The post-war settlement suited the post-war population. Beveridge built for a country where most people died within a few years of stopping work and many workers stood behind each retiree. Both halves have inverted.

People now spend two or three decades in retirement while the supply of workers beneath them collapses.

The Office for Budget Responsibility expects the old-age dependency ratio to climb from 31 per cent to 47 per cent over the next fifty years. On current policy it projects borrowing above 20 per cent of GDP and debt above 270 per cent by the early 2070s, naming the rising state pension as a leading cause.

Pensioner benefit spending already runs near £138 billion a year and is forecast to rise by roughly £31 billion more by the end of the decade. The state pension alone now takes about 5.3 per cent of national income, the highest share ever recorded. Off the official books sit some £1.4 trillion in unfunded public service pension liabilities, a figure large enough to make the visible ones look quaint.

Every available repair breaks one of the promises the system was built to keep.

| The fix | The promise it breaks |

|---|---|

| Raise the pension age | Retirement at a knowable age |

| Cut payments | A dignified old age |

| Raise taxes | The working-age compact |

| Import workers | The national compact |

| Borrow more | The compact with the unborn |

| Means-test it | The contributory myth |

Reform never settles anything. Each adjustment shifts the pain from one bloc of voters to another and waits for the complaints.

The cleverest repair has been demographic: if there are too few workers beneath each retiree, import workers. The OBR says exactly this in dry language, noting higher net migration improves the dependency ratio because migrants skew towards working age.

Stop here for a moment. Understand what is being said, and what has happened. This is what the OBR says and the Treasury believe:

The conclusion we draw from these projections is that because the age structure of inward migrants to the UK is skewed towards those of working-age, net migration reduces the dependency ratio over our 50-year horizon and thus reduces age-related pressures on the public finances.

Read plainly, it is an admission that an unfunded promise can only be kept by continually importing the workers to pay for it, decade after decade, with no end state in which the books ever balance. The fault lies in the design, not in the people who answer the advert. A funded system removes the fiscal incentive for any government to treat migration as a substitute for family formation, capital accumulation and the productivity of care. Build the capital honestly and the demographic transfusion is no longer load-bearing.

None of this means abandoning the elderly. It means being honest about what they were actually promised, and building machinery that does not need a permanent demographic transfusion to stand up.

Four Things Hiding Inside One Word

"Pension" hides at least four jobs pretending to be one, and the moral weight is not spread evenly across them.

- There is a poverty floor that stops old people falling into destitution.

- There is saving, the simple business of setting money aside while you earn so you have something to live on once you stop.

- There is insurance against the genuinely unpredictable, chiefly the risk of outliving your money.

- And there is a political entitlement, the universal payment handed to everyone above a certain age regardless of need, because pensioners vote and governments are weak.

Only the first carries an unconditional moral duty. No decent society lets its old starve. The second is work that ordinary saving does well, given honest accounts and time for the money to grow. The third is a true insurance problem, solved by pooling.

The fourth is not a duty at all; it is a bribe wearing the clothes of the other three.

Separate the bundle and the design opens up:

- Fund the floor from tax.

- Build the savings as real money you own.

- Insure the long-life risk through a pool.

- Stop pretending the bribe was ever a sacred contract.

The framework which follows does precisely these four things, and then adds the part every cash scheme ignores: the place, the people and the care that money alone never buys.

Where Dark Lord Blair Stops Short

The Tony Blair Institute deserves credit for saying the unsayable: its Lifespan proposal accepts the state pension should be replaced rather than endlessly re-uprated, swapping it for a flexible lifetime income-support account people could draw on across the course of their lives, with earlier access for things like retraining, unemployment or caring.

That is a real advance on the usual cowardice, and the longevity-pooling instinct behind it is sound. But it remains a better-administered cheque. It asks how to make pension spending sustainable.

The deeper question is how to end the intergenerational deception altogether and rebuild the institutions whose disappearance left old age so bleak.

A lifecycle account, however cleverly flexed, still leaves the widow alone in her terrace with a payment and a list of unanswered questions. It funds the subsistence and ignores the abandonment. The Commonwealth Society funds both, because it is not a payment at all.

The Structure Of The Replacement

The Commonwealth Society Framework rests on four pillars. Three of them are financial layers that replace the state pension's money function. The fourth is an institution which replaces what the state pension never even attempted: a later life worth living.

- The Citizenship Floor is the honest poverty net, paid from general taxation to any long-term citizen who reaches later life without enough to live on. It is welfare, openly labelled as welfare, and it follows the person.

- The Personal Capital Account is real, owned, invested money built across a working life. It replaces the fiction of "I paid in" with the fact of it.

- The Dependency Pool is mutual insurance against the costs of care and of living far longer than expected, the risks no individual account can carry alone.

- The Commonwealth Society is the physical institution where these meet: a small, beautiful, member-owned settlement that people join while still well, contribute to for years, and age into among people who know their names. It provides fellowship, housing, on-site care, final provision, and help for the family afterward.

The state supplies four things and no more: land, law, tax shelter, and the last-resort floor, each on terms set out below. It never operates a single Society. And the ordering matters, against the obvious misreading.

The three financial layers are not the settlement; they are its plumbing. The Account is not the destination, it is what feeds the Society.

The point of building the capital is to build the place, the care and the fellowship the capital then pays for, so nobody arrives at old age holding a pot and facing the void alone.

Layer One: The Citizenship Floor

We start with the floor, because it is the part which carries the genuine moral obligation and the part most easily misrepresented as cruelty.

Every lawful long-term citizen or resident who reaches later life without sufficient income receives a basic payment sufficient to prevent destitution. Not middle-class comfort. Destitution-prevention, openly and honestly. The crucial change from the present system is not the amount but the label. The Floor is welfare. It is funded from general taxation rather than the National Insurance fiction. It does not pretend to be an earned annuity, because the lie it was earned is what made the whole settlement impossible to reform.

The Floor is means-tested against income and liquid assets, with sane protection for a primary home up to a regional cap, so a widow in a modest terrace is not stripped of her house to qualify. It rises by a statutory formula tied to median wages and a basic basket of living costs. It is emphatically not triple-locked, because the triple lock is the purest example of the political bribe: an uprating rule with no actuarial logic, designed to win the votes of the people most likely to cast them.

The Floor absorbs the present tangle of pensioner add-ons:

- Pension Credit, the means-tested maze one in three eligible pensioners never claims, folds into it.

- The winter fuel payment, that perennial political football, folds into it.

- The scatter of micro-benefits which exist only because the main system is incoherent fold into it.

One honest payment, one means test, one statutory formula, replacing a thicket grown to disguise the fact that the universal pension was never enough on its own.

The moral line holds in one sentence. No elderly person is abandoned, and no working family is taxed into poverty to sustain a pretence.

Layer Two: The Personal Capital Account

This is the part that makes "I paid in" true at last. Every worker holds a Personal Capital Account: real money, legally owned by the individual, invested and compounding across a working life. Not a notional entry in a government ledger. Not a claim on future taxpayers. An actual account with an actual balance, beyond the reach of any Chancellor who fancies raiding it to fill a Budget hole.

It is built from four streams.

- The employee contributes.

- The employer contributes.

- The family may contribute, and this is no afterthought: an adult child can pay into a parent's account, a parent can seed a child's.

- And the state tops up the accounts of those whom the labour market underpays for socially valuable work: low earners, carers, parents of young children, the disabled, those who have served in the forces.

The state stops pretending everyone's market wage reflects their worth and credits the contributions society actually depends on.

The vital point about the contribution is almost none of it is new money. The account is fed by redirecting flows which already leave a worker's pay packet or sit in their name, gathered into one place they own. Current auto-enrolment contributions flow in. The employer's existing pension contribution flows in.

The portion of National Insurance which today funds the state pension is redirected here rather than spent the same week, though, as the transition section explains, this redirection happens gradually, so that the promises already made to current pensioners go on being funded separately while new contributions begin to build. Existing pension tax relief attaches to the account.

To these are added state top-ups for socially valuable work, transfers from private pensions, the value of service credits, housing equity released late in life, and legacy gifts from family.

The headline percentage looks large only because it consolidates streams that are presently scattered, hidden in employer accounts, or swallowed by a pay-as-you-go system that leaves nothing behind.

A worker is not asked to surrender a fifth of their wages on top of everything they already pay. They are asked to let the money already moving through the system land in an account with their name on it.

Even so, the ambition should be real, because timid saving is how Britain arrived at its present poverty of provision. Singapore's Central Provident Fund gathers a combined 37 per cent of wages for younger workers. Britain need not match that, but a consolidated rate well above the 8 per cent floor of current auto-enrolment is the order of magnitude that produces genuine capital rather than a token. A worker whose redirected contributions compound from their twenties, with employer match, arrives at later life holding a six-figure account rather than a weekly handout.

The default investment is a small number of low-cost national index funds, the same broad-market vehicles which have quietly turned ordinary savers into people of substance over working lifetimes. Inertia is designed to work in the saver's favour: do nothing and your money sits in a sensible, cheap, diversified default rather than being skimmed by a salesman.

Those who want to choose a private provider may, but the path of least resistance leads somewhere good rather than somewhere expensive.

At retirement the account does not simply hand over a cheque to be spent or lost. A minimum portion must convert into lifetime income, through an annuity, a programmed drawdown, or a hybrid, so nobody can blow the fund at sixty-eight and fall entirely onto the taxpayer at seventy-eight. Above that floor of secured income, the rest is genuinely yours, to spend, to give, or to leave.

And here the account does something the state pension could never do: it passes on.

Whatever remains at death flows to a spouse, then to children. Not everyone will leave a large sum, because care is real and has to be paid for, and a long decline can eat a good deal of an account. But the difference from the state pension is the difference between something and nothing.

The state pension vanishes the week you die, by design; there is no balance, because there was never an account.

Here, what you did not need is what your children inherit, and across two or three generations of careful families that builds into the thing Britain's working people have been denied for a century: real capital of their own, handed down rather than handed back.

Layer Three: The Dependency Pool

Two risks defeat any individual account, however well funded. You cannot know in advance whether you will need years of expensive care, and you cannot know whether you will live to eighty-three or a hundred and three. These are insurance problems, and insurance problems are solved by pooling, not by saving.

The Dependency Pool is mutual longevity-and-care insurance, contributed to from the Personal Capital Account during working life and pooled across all members of all Societies. It does two jobs.

- It pays for care when a member crosses from independence into needing daily help, and

- It tops up or takes over when a member outlives the income their own account can sustain.

Structure the maths honestly and the tail is far cheaper to guarantee than the universal payment it replaces.

Most people die before they draw heavily on extreme old age; the pool only pays out for the minority who live longest, which is exactly why pooling works.

Let personal capital fund the predictable middle of retirement, where saving does the job perfectly, and let the pool insure only the genuinely unpredictable extremes: the catastrophic care need and the very long life.

The state stands behind the pool as the final backstop, stepping in only if some shock hit everyone at once, but it does not run it and does not pretend to owe everyone an indefinite income regardless of their own provision.

This single change retires an absurdity.

Today the state is simultaneously pension provider, poverty charity, annuity company, inflation insurer, demographic engineer, and electoral bribe machine, performing every one of those roles badly because they contradict each other.

The Floor handles poverty. The Account handles smoothing. The Pool handles the tail. Each does one job, and each can therefore be costed, run and judged on its own terms.

What Britain Had Before The State Took Over

None of this is invention. It is recovery, and the thing being recovered was once one of the largest features of British life. Before the welfare state, ordinary people did not face misfortune alone or wait for a ministry to rescue them. They joined together and built institutions to carry one another, and those institutions were vast.

The Marxist revisionist history of this period is staggeringly dishonest. The world was not a crushing soulless dystopia. Answers to problems evolved through British community and ingenuity.

The friendly societies were the heart of it. By the early twentieth century they counted their members in the millions, more people than the trade unions and the chapels, working men and women paying a few pence a week into bodies they themselves owned and governed. A society paid you when you were sick, kept your family when you could not work, and buried you when you died, the burial clubs sparing the great Victorian dread of the pauper's grave. They held halls, ran clubs, kept libraries, met in their own rooms.

The Oddfellows, the Foresters, the Hearts of Oak: names half-remembered now, but once the everyday machinery by which a free people insured itself against the blows of life without surrendering its independence to the state or its dignity to charity. The trade guilds had done something similar for centuries before, and the co-operative movement, born in Rochdale, carried the same instinct into retail and finance and housing.

What they shared was a form. They were:

- Mutual, owned by their members rather than by shareholders or the state.

- Local, rooted in a place and a trade and a face-to-face membership, and

- Comprehensive in a way no single benefit ever is.

They did not hand out a payment and walk away, they wove a person into a body that knew them and would act for them.

Then the state arrived, and it did not absorb this world so much as hollow it. It nationalised the parts which could be funded from taxation, the sick pay and the pension and the burial money, and in doing so removed the reason to belong.

Why pay into the Oddfellows when the state now did the paying? The societies withered as their function was stripped out, and the survivors, the building societies and mutual insurers, were later demutualised in a wave of windfall payouts which handed the accumulated capital of generations to whoever happened to be a member on the day, and converted institutions built to last centuries into ordinary banks that mostly failed within decades.

The civic, owned, comprehensive thing was replaced by two colder things on either side of it: an impersonal state benefit, and a market in which old age became a product sold back to you at retail.

The Commonwealth Society is that lost form, hardened against the failures which killed it the first time and pointed at the one domain where its disappearance hurt most. Old age is precisely where a cheque and a market both fail, and precisely where being woven into a body that knows you matters most.

The name is chosen with care. "Commonwealth" here means neither empire nor ministry. It means common wealth, in the old English sense: things of value held in common, across generations, for a shared human purpose.

A common wealth is called a society or common doing of a multitude of free men collected together and united by common accord and coveanauntes among themselves, for the conservation of themselves as well in peace as in warre.

Not owned by the state, not owned by shareholders, but owned by the people who belong to it and held in trust for those who will belong to it next. That is exactly what a friendly society was, and exactly what this is.

The Commonwealth Society Itself

A Commonwealth Society is a small, member-owned community you join while you are still well, pay into for years, and one day live in. It is not a care home.

A care home is where you are sent once everything has already gone wrong, among strangers, at the worst moment of your life.

A Society is somewhere you choose, early, while you are healthy enough to enjoy it and help shape it. It has homes for its members, a doctor and carers on site, a dining room, gardens, workshops, company, and a settled way of handling things when you die and after. One place holds the whole of it, from your first Sunday lunch there at fifty to the sorting of your affairs once you are gone. Nobody has to assemble it in a panic, because it was all arranged long before you needed it.

The thing to understand here is what the Society is for, not its registration: a body which holds the whole of later life in one place, owned by the people it serves.

What the Society sells is not care, and not even housing. It is foreseeability.

At forty the real fear is not a number but a set of questions the current system answers with silence: where will I go if I am widowed, who will notice if I stop eating, what happens when I fall, who deals with the house, where do I die, what chaos do I leave behind.

The state pension answers all of them the same way. Here is a payment; manage. The Society answers them years in advance, by being the place where those questions already have answers before you ever need them.

Who Can Start One, And How It Is Registered

The plainest questions deserve plain answers. Who is allowed to build one of these, and what stops anyone from hanging up a sign and calling a boarding house a Commonwealth Society?

Almost anyone may start one, and that is deliberate, because the strength of the old mutual sector was that it grew from below rather than being handed down. A group of founders, a parish, a trade body, a faith community, a charity, a town that wants one, even a circle of friends in their forties who would rather shape their own old age than gamble on the state's, can come together and form a Society.

They register it under the existing law, the Co-operative and Community Benefit Societies Act 2014, which already provides a body which trades for the benefit of a community rather than for members' profit and can adopt a statutory asset lock so its corpus can never be sold off or demutualised. Community pubs and land trusts use this shell today. It is sitting in the statute book, tested and ready.

"Almost anyone" is not "anyone with a leaflet", though. Before a Society can draw on tax relief, public land or the guarantee, chartering requires it to show its working: a viable plan for how it will fund itself, named and accountable trustees, proper governance and audit arrangements, and safeguarding in place before a single vulnerable person walks through the door.

Five enthusiasts with good intentions and no plan do not get the keys to public money. The gate is open, but you have to prove you can carry what is behind it.

But the name is protected, and the protection is the gate. Calling yourself a Commonwealth Society, and claiming the advantages which come with it, the tax shelter, the access to public land, the public guarantee behind the dependency cover, is conditional on accepting the charter that defines one.

That charter is not optional decoration. It requires the asset lock, the cap on size, the mixed membership with its minimum share of floor-supported members, the statutory duty of beauty, the internal walls between care and money, the guardianship protections, the open accounts, and the seven anti-capture rules set out later.

A body that will not accept those terms is welcome to operate as an ordinary care home or retirement complex under ordinary law. It simply may not wear the name or draw on the public support, because both are reserved for institutions that have bound themselves to the obligations that justify them.

Regulation, then, works in two layers rather than through one heavy inspectorate.

- Registration and the charter are the front gate: a Society is chartered only if its constitution contains the locks.

- Conduct afterward is policed mostly through enforceable rights rather than a standing bureaucracy, the member powers, family and advocate rights, funding withdrawal, the fast tribunal, criminal law and automatic intervention triggers detailed below, with a single narrow statutory inspector for safeguarding against abuse and neglect.

The rule throughout is minimal regulator, maximum enforceable rights. Easy to start, hard to corrupt, and impossible to fake without forfeiting the very things which make it worth faking.

How The Land Is Found

Building a national network of Societies needs land, and land is where good intentions usually meet either expropriation or extortion. The framework's land doctrine is simple and avoids both. Public and quasi-public land comes first: redundant council holdings, surplus NHS estate, Crown Estate parcels, the considerable stock of underused public land which currently sits idle or is sold off to the highest bidder for executive flats. This is offered to Societies on long leases at values reflecting its civic use rather than its speculative ceiling.

Where private land is converted for a Society, the planning uplift is captured. A field worth little as agriculture and a fortune with permission should not hand its owner a windfall at the public's expense; the gain from rezoning is shared, funding the Society rather than the speculator.

And private land may enter voluntarily, on ordinary terms: sold, leased, gifted by legacy, or brought into partnership by a landowner who would rather see a Society on the family acres than another distribution shed. Church land and charitable estates, much of it already held for something like this purpose, can join the same way.

No compulsory seizure of family farms, no green-belt free-for-all, no Whitehall land bank. Public land put to public use, private uplift shared where permission creates it, and voluntary entry for everyone else.

The state makes land available. It does not confiscate it.

Tax That Shelters Provision + Punishes Extraction

The tax system already pours relief into private pensions, on the principle money locked away for old age should not be taxed on its way in or while it grows. The framework takes that principle and points it at the whole of provision rather than at a pot alone.

A private pension earns relief for building a sum of money. A Commonwealth Society should earn the same treatment for building the place, the care, the fellowship and the final provision that the money would otherwise have to buy at retail, often badly and at the worst possible moment.

The formula is short.

- Contributions in are deductible or tax-neutral, whether they come from the worker, the employer, the family or a transferred pension.

- Growth inside the Society is sheltered, exactly as growth inside a pension is.

- Land brought into locked later-life use attracts relief.

- Legacies committed to locked later-life provision are inheritance-tax favoured; ordinary inheritance of whatever capital remains passes under the rules Parliament sets, with the usual anti-avoidance limits, so that a Society cannot be used as a pipe to wash an estate past the taxman.

- Provision drawn down as care, housing and fellowship is tax-free at the point of use.

And then the hinge, the part which makes the shelter safe to grant: any extraction from the locked purpose is taxed hard and penalised.

The reliefs attach to provision that stays locked for what it was meant to do. Money pulled back out for some other end loses every advantage and pays a penalty on the way.

This is what stops the tax shelter becoming a tax dodge, a way for the comfortable to launder an estate through a pretend Society. Relief follows locked provision, never institutional fashion and never the cleverness of an accountant. The state shelters what is genuinely committed to later life, and claws back hard from anything which tries to escape the commitment.

This also answers the Treasury's complaint before it is made.

Yes, this is tax expenditure, transition borrowing and public land put to use. But set against an unfunded pension liability and a social-care bill which grow without limit, it is not new spending so much as the conversion of an open-ended future claim into a bounded present investment.

The question was never whether the state pays. It is whether the state pays forever into consumption, or once into institutions which reduce the claims upon it for generations.

Beauty As A Legal Duty

If these places are ugly, institutional, cheap and joyless, the model collapses, because nobody well chooses to live somewhere grim, so the only entrants are the desperate, so the Society degrades into the warehouse it was meant to abolish.

Beauty is recruitment, prevention and dignity at once. It cannot be left to the goodwill of developers, so it becomes a statutory duty written into the founding purpose.

The law obliges each Society to create and maintain places of beauty, domestic scale and civic belonging, fit for free citizens to choose before they need anything. In practice that requires human-scale buildings, gardens and trees and courtyards, natural light, proper dining rooms, workshops and libraries and quiet rooms and cafés, guest rooms for visiting family, and local materials where they can be had.

It forbids warehouse corridors, institutional décor, tower-block storage of the old, and the minimum-viable-care-box architecture which disfigures the present sector.

Beauty in law sounds subjective, so the duty has to be made justiciable without collapsing into design-by-committee. The way to do that is to fix the things which can be tested and leave the rest to local judgement.

A Society's buildings must meet measurable standards: domestic scale rather than institutional bulk, minimum garden and open-space provision, natural light in living quarters, walkable internal layouts with no warehouse corridors, shared dining, and guest accommodation for visiting family.

Each Society's plans are approved against a local design code by an independent architectural jury drawn from the locality rather than appointed in Whitehall, and members vote periodically on whether the place they live in is, in fact, a place worth living in. The objective floor stops the cheap warehouse; the local jury and the member vote stop the bland template.

The test is one sentence, and a Society that fails it has failed its purpose regardless of what its accounts say. Would a sound-minded sixty-eight-year-old choose to live here before they needed care?

Membership: A Future You Vest Into

The obvious abuse is the late arrival who joins at sixty-four, contributes for a fortnight, and expects thirty subsidised years of beauty, food, company and care. A serious institution cannot allow it, so membership vests over time rather than switching on at a magic age.

You do not buy a room when you are frightened. You spend years helping build a place where you will one day be known.

Membership runs along a ladder, and a person can stand on it for decades before drawing anything heavy.

| Membership duration | Rights earned |

|---|---|

| 0–5 years | Social access: lunches, gardens, clubs, lectures, advice. Services at cost. No deep subsidy. |

| 5–10 years | Partial fee reduction, some priority, limited final provision. |

| 10–15 years | Strong access rights, partial dependency support. |

| 15+ years | Full vested membership: housing, care, final provision, estate support. |

Fifteen years to full vesting is the natural figure.

With later life beginning around sixty-five, it sets the latest ordinary joining age at fifty and gives every Society a genuine capital base built years before the heavy costs land.

A social member can join at any age, pay ordinary dues, and belong to the life of the place long before they need anything from it, which is precisely how the capital and the community both accumulate.

Starting late cannot mean exclusion, though.

A widow arriving at fifty-eight should not be locked out for life, even if she cannot have the terms of someone who paid in from thirty-five. Late entry stays open through a larger capital contribution, a transferred private pension, a charge against her housing equity, a family contribution, a legacy commitment, a higher fee, or the Citizenship Floor where she is genuinely poor, with benefits limited until she vests.

The rule cuts both ways and is fair in both: late entry is allowed, full subsidy is earned.

Service is contribution too, and this matters most for those with the least money. The member who drives the minibus, teaches the apprentices, cooks, gardens, mentors or keeps the place running earns standing through labour.

A poorer member pays in hours where a richer one pays in pounds, and the Society values both, because a community runs on both.

Turning A Private Pension Into A Place

Millions of people approach later life holding not a state promise but a private pension pot, built through decades of workplace saving, and the framework has to give them a door in or it simply concedes the field: Societies for those who arrive with nothing, private pensions for those who saved, and the two-tier world the whole design is meant to abolish.

A private pension can be exchanged, in whole or in part, for membership. The mechanism is a straight conversion of capital into standing.

A pot transferred into a Society buys a lifetime reduction in fees, priority for housing, dependency cover, final provision, spouse protection and the estate-resolution package, the same bundle a long-vesting member accumulates through years of contribution, purchased instead with the capital already saved.

A man of sixty-two with a respectable pot and no particular wish to manage drawdown and annuities and care insurance separately for the rest of his life can fold the lot into a single membership answering all of it at once, and know his wife is provided for in the same act. The pot stops being a number he watches anxiously and becomes a place he belongs to.

This is also what stops the framework being outflanked.

The saver is not punished for having saved, nor left outside the new settlement clutching a pot while the propertyless are housed. The state pension, the private pension, and the Society cease to be three separate worlds for three separate classes. They become three roads to the same front door.

And the wealthy have their own reason to walk through it, one that has nothing to do with running short of money.

The comfortable retiree with a large pot and a paid-off house is not protected by any of it from the things that actually make old age frightening. Money does not stop a husband dying. It does not fill the silence of a house when the children live abroad. It does not notice when you have stopped eating, or catch you when you fall, or shield you from a care chain which sees you as a margin, or spare your family the chaos of a death nobody prepared for, or arrange you die among people who know your name.

The rich man dies alone just as surely as the poor one, and rather more often, because money buys the very isolation, the big detached house, the privacy, the independence, the end of life turns into a trap.

The Society offers him what his wealth cannot: not provision, which he has, but belonging, which he cannot purchase at retail.

That is why a serious model is not a charity for those who failed to save. It is a better answer to old age than money alone has ever managed to be.

Who Pays For What, And When

Strip away the warmth and the financing has to work pound for pound. It does, through the three layers meeting at one body.

- A vested member pays a fee, drawn first from their own Personal Capital Account.

- When they cross into needing care, the Dependency Pool covers it.

- Where a member is genuinely poor, the Citizenship Floor follows them in and pays their way.

- The building itself is asset-locked and can never be sold from beneath the people living in it, which is also exactly what keeps the private-equity buyer out.

The same predators currently extracting margins from children's placements and nursing homes find there is nothing here to buy: the fee purchases a life and the care comes with it, never a share anyone can cash out.

The hardest case is the ordinary middle, neither destitute nor rich, and the whole financing claim stands or falls on solving it.

A widow of seventy-nine owns a paid-off terrace worth two hundred thousand pounds and holds almost no cash. She wants to move into the supported tier of her Society. Her only real asset is the house, and a house liquidates cleanly only when she sells up and leaves, which is the precise upheaval the whole arrangement exists to spare her.

The answer is an estate-backed charge. The Society advances the cost of her care against the value of her home while she goes on living wherever she chooses, in her terrace or in a cottage on the Society's land, registering a charge rather than forcing a sale. She keeps her home and her settled life. The charge accrues quietly. When she dies, it is discharged from her estate, and whatever remains passes to her heirs.

This is the strongest financing idea in the framework and also the most easily caricatured, as a dementia tax, an inheritance raid, a slow house grab by an institution waiting for an old woman to die.

It is hedged about with hard protections, and the protections come before the charge, not after.

- A spouse or dependant living in the home is shielded; the charge cannot displace them.

- Recoverable costs are capped, the fee schedule is published, and interest, if any, is simple rather than compounding, so the debt cannot balloon into usury while the member sleeps.

- Independent advice is mandatory before anyone signs, paid for outside the Society so the adviser has no stake in the answer, and a cooling-off period follows.

- A regional floor of home value is protected for the heirs wherever the equity allows.

- The charge is portable, so a member can move to another Society and take the arrangement with them, and it is reviewable by a tribunal if anything about it is contested.

- When the equity is genuinely exhausted, the member does not lose their place; the Dependency Pool and, beneath it, the Citizenship Floor carry them on.

Two further rules guard against the fear the first friendly lunch is the thin end of a property pipeline.

- A Society cannot require an estate-backed charge as a condition of ordinary social membership; you can belong, eat, attend and build standing for years without ever signing anything against your home.

- Any estate-resolution function is optional and separately substitutable, unless the member chose it explicitly while competent; the body which funds the care does not thereby acquire an automatic grip on the settling of the estate.

The principle is stated plainly so nobody mistakes it: the house funds the care arc only after the person, their spouse and their dependants are protected, and only when the member has genuinely chosen it. The Society is not waiting for the house.

Probate then falls out almost for free.

A body which has held a charge against the principal asset throughout the care years is the natural body to settle the estate at death, clear its own charge, and pass the residue to the family, with an estate-resolution service attached.

The present horror, in which asset and liability are torn apart and a grieving family meets the open market alone, is healed because one institution has held both ends the entire time.

The Society Coordinates The Arc; It Does Not Own The Life

The emotional power of a single body holding the whole arc carries an obvious danger. A body which controls a person's housing, their care, their money, their funeral and their estate could become the most frightening institution in their life, especially for the member who has lost capacity or has no family to watch on their behalf.

The framework answers this with internal walls, not pious hope. The Society coordinates the arc. It does not own the member's life.

- The walls are structural. The functions which could otherwise collude are kept apart: housing governance, clinical care, financial accounts, and estate resolution are separate domains within the Society, separately accountable, so the people deciding a member's care are not the people who profit from the charge on their house.

- Above all, the member holds exit and substitution rights. They can take their financial account elsewhere, appoint an outside executor, choose a different funeral provider, or move to another Society entirely, carrying their charge and their vested standing with them.

- The Society is the anchor, not the proprietor. A member is a free citizen who has chosen this place, and can unchoose it.

The hardest version of the problem is the member who can no longer choose: the one who has lost capacity, and the one who has nobody. The framework meets it with civic guardianship, built on a single rule that admits no exception.

The institution providing the care cannot be the sole guardian of the person whose estate funds that care. The financial interest and the welfare decision must sit in different hands.

When a member loses capacity, an independent advocate is appointed from outside the Society, with standing to scrutinise care decisions, challenge any move to extend or enlarge the estate-backed charge, and refer concerns to the tribunal.

For the kinless member, who under the present system is the most exposed person in the country, the advocate is not an optional extra but the default, a civic guardian whose entire job is to be the watching relative the member does not have.

Guardians are themselves reviewed, on a register, removable for cause, never permitted a financial interest in the estate they oversee. Care decisions are challengeable, by the advocate, by family, by other members.

The chain of people who could quietly take advantage of a confused old person is broken at every link, by design, because the whole moral claim of the framework collapses if the demented and the alone are not safe inside it.

The End Of Life, Held By One Institution

The state pension stops at the worst possible moment and leaves everything else to chance. The payment ends the week you die, and the rest, the funeral, the house, the probate, the grief, the bureaucracy, lands on whoever loved you, usually all at once and usually badly.

Britain has built an entire dismal economy around this failure: the funeral debt, the probate solicitor billing by the hour, the distressed sale of a half-empty house, the storage unit of a parent's belongings nobody can face.

A Commonwealth Society absorbs the whole of it, because it is the one body which has known you for years and can hold your affairs already. Final provision is part of vested membership, not an extra to be purchased in a panic.

- The funeral is arranged according to wishes you recorded long before, in the manner and the faith you chose, paid for from provision built up across your membership rather than borrowed against by a shocked relative.

- The burial or cremation, the service, the wake in the dining room where you ate for twenty years, all of it sits inside the Society rather than being outsourced to a chain which scents desperation.

- Many Societies will hold their own burial ground or memorial garden, the burial-club instinct of the old mutuals restored, so members rest in the place they belonged to rather than in an anonymous municipal plot.

The estate is settled by the body which financed the care and held the charge. There is no handover to strangers at the moment the family is least able to manage one.

The Society's estate-resolution service discharges its own charge first, transparently and on published terms, then administers the residue: the house dealt with in good order rather than dumped on the market in the first grief-struck month, the accounts closed, the belongings handled with the dignity of people who knew their owner. What remains in the Personal Capital Account passes to spouse and children.

The Society has every incentive to do this cleanly and none to bleed the estate, because its charge is fixed and its conduct is watched by members, family and the tribunal alike.

The family is carried through it rather than abandoned to it.

Guest rooms mean relatives can stay in the final days rather than commuting to a hospital ward at the end of a motorway. The community which knew the member grieves alongside the family rather than leaving them to grieve alone. Bereavement support is part of what the Society does, because a body built around belonging does not switch off its care at the graveside.

The contrast with the present settlement is total.

Today a death triggers a scramble; under the framework it triggers a process the deceased themselves helped shape, among people who knew them, with the money already provided and the affairs already in hand.

This is the part the cash systems cannot touch at any contribution rate. A larger weekly payment does not arrange a funeral, sit with a widow, clear a house or settle an estate. Only an institution that has held the whole arc can do that, and holding the whole arc is precisely what the Commonwealth Society is for.

The Framework Against Real Life

Specification is hollow until it survives contact with a real life. Walk through the events that actually frighten people, and watch how the framework answers each.

You join at forty-eight, healthy and working

You become a social member of a Society near where your children are putting down roots. You pay modest dues. You use the dining room on Sundays, you join the woodworking group, you start to know the older members who will one day be your neighbours. Your Personal Capital Account, running since your twenties, is now well into six figures and compounding.

You have done nothing dramatic. You have simply started belonging to the place where your last chapter will unfold, and the low background dread that used to attach to the words "old age" has begun, quietly, to lift.

Your husband dies when you are seventy-one

Under the old settlement this is the moment the floor gives way: the house too big and too empty, the income halved, the long evenings alone, the slow slide toward a crisis that ends in whatever care bed happens to be free. Under the framework you are a vested member of fifteen years' standing.

There is a flat waiting in the Society if you want it, a dining room where you are known by name, a community that notices when you do not come down for breakfast. You are not relocated among strangers at the worst moment of your life. You move, if you move at all, toward people who already know you.

You fall and cannot manage alone

You cross from independence into needing daily help. There is no scramble for a placement, no frantic ringing round of homes, no children taking unpaid leave to navigate a system designed to exhaust them.

Care begins where you already live, funded by the Dependency Pool, delivered by people who know your history because they have known you for years. The estate-backed charge covers what your account cannot, against your home, without forcing its sale.

You develop dementia

This is the case which breaks families and bankrupts estates under the present system. In a Society the care is on site, continuous, and provided by a body that loses money if it neglects you and is watched by members, family and a fast tribunal if it does.

The moment your capacity fails, an independent advocate from outside the Society takes up your corner, empowered to question your care and to block any attempt to enlarge the charge on your home while you cannot speak for yourself.

The people who decide your care are walled off from the people who hold your money.

Your family can stay in the guest rooms. You decline among people, in a place built to be beautiful, watched over by someone whose only job is your interest, rather than alone in a house that has become a hazard.

Your money runs out before you do

You live to ninety-six and your Personal Capital Account, sized for a normal retirement, is spent. This is the longevity tail, and it is precisely what the Dependency Pool exists to catch. Your secured income continues.

Your place in the Society does not depend on your bank balance, because the pool, not your dwindling savings, now carries you. You are not evicted into the state system at the very end. You stay.

You die

Your funeral is not a panic visited on shocked relatives. The Society has a process, and your wishes, recorded years earlier, are known. The estate-backed charge is discharged.

The estate is settled by the body which financed your care and held your affairs, cleanly, without your children meeting a probate solicitor and a distressed property market in the same grief-struck month. Whatever remains in your Personal Capital Account passes to them. You leave clarity behind you, and very possibly capital.

You are poor your whole life

You never accumulated much; your work was care and cleaning and kindness rather than salary. The Citizenship Floor pays your way into a Society, and your years of service, the minibus and the kitchen and the mentoring, earned you standing the rich member bought with money.

You age in the same beautiful place, among the same community, with the same care. The framework does not have a wing for the deserving and a shed for the rest. The floor is real, and it leads to the same front door.

You have nobody

No spouse, no children, no one to notice or to act. Under the present system you are the most exposed person in the country, the one who dies undiscovered and is buried by the council.

In a Society you are precisely the person the design is built around. You belong to a community that notices your absence at breakfast. When your capacity fails, a civic guardian is appointed by default, an independent advocate whose whole purpose is to be the relative you never had, watching your care and guarding your estate against the institution that holds it.

Being alone stops meaning being unprotected.

Your body gives out before the calendar says it should

You laid bricks, or lifted patients, or stood on a warehouse floor for thirty years, and at fifty-eight your back and your knees are finished while an office worker your age has another decade in them. The framework distinguishes the end of physical labour from a chronological age printed on a form.

Demonstrable physical incapacity opens early access. Retraining and mentoring credits let you move to lighter work or to teaching your trade to apprentices inside a Society, earning standing through the knowledge in your hands rather than being thrown on the scrapheap.

The worn-out worker is not made to wait, pretending to be fit, for a pension age designed around people whose work never touched their bodies.

Standards Without A Single New Quango

All of this invites the reflex objection: such a system needs a vast inspectorate to police it. It does not, and building one would betray the design, because a remote regulator with a scheduled visit is exactly the dead hand of the hollowed out care sector it was meant to guard.

Enforcement comes instead through five things that bite harder than a clipboard: rights, money, courts, insurance, and the freedom to leave.

Members hold real legal powers

They can inspect the accounts, call extraordinary meetings, elect and remove the board, trigger independent audits, vote no confidence, and petition for transfer or administration. The board answers to the people it serves, not to a ministry. Families, guardians and advocates can act for those who cannot act for themselves, triggering a safeguarding review, a care-quality investigation, a financial audit or a court action.

The money follows the member, not the institution

The Dependency Pool and the Citizenship Floor can suspend new payments to a failing board, redirect the money through a temporary administrator, or fund a member's transfer to a better Society. This is the sharpest lever of all, and it is aimed at the management rather than the residents: the cash keeps reaching the people who need care, through an administrator if necessary, while the board that failed them is starved and replaced. A body protected by the state can limp along neglecting people for years; a body whose money walks out of the door with its members cannot.

A dedicated court tribunal, fast and cheap and local

Rather than a sprawling agency, it can remove directors, appoint temporary administrators, block the misuse of assets, compensate members, order transfers, and refer fraud or abuse for prosecution. In urgent cases it can act the same day: restoring a family that has been shut out, moving a member to safety, freezing the accounts, or putting an interim administrator in charge that afternoon. When someone is being hurt, the response is measured in hours, not in the months a conventional inspection regime takes to schedule a visit.

Societies inspect one another, on rotating assignment, with the reports made public. External eyes without a permanent regulator class.

And certain failures trigger intervention automatically, with no official discretion to look the other way:

- unexplained deaths;

- repeated falls;

- financial irregularity;

- staffing below declared levels;

- failures of food or heat;

- blocked family access;

- abuse allegations;

- refusal to publish accounts, and

- any attempt to shift assets or sign related-party contracts.

Open books, member power, insurer discipline, and a court which can move quickly frighten a bad operator far more than an inspection regime that telephones ahead.

Inspection cannot be avoided

Honesty requires one concession. A body which provides nursing, dementia care, medication and palliative support cannot be left entirely to member councils and peer review, because some of its residents will be incapacitated, kinless or afraid, and those are exactly the people member democracy serves worst.

There remains a single statutory inspector, with a deliberately narrow remit: safeguarding against abuse and neglect, nothing more. It does not set fees, dictate design, license providers or accumulate the thousand secondary functions through which inspectorates grow into empires.

The doctrine is minimal regulator, maximum enforceable rights. The clipboard exists, but it is small, and the real teeth are in the hands of members, families, insurers and courts.

Smallness Is The Whole Defence

The housing association sector is a warning written in its own history, because it began precisely where this framework begins. They began as charitable projects in Victorian times, like the friendly societies.

Small, local, mission-rooted bodies consolidated over decades into national giants owning a hundred thousand homes, took on commercial debt, spun up profit-making subsidiaries which bent the asset lock, and produced governance and care scandals once sheer scale put distance between the board and the resident.

The defence is to make smallness permanent rather than a passing phase.

An unlimited network of Commonwealth Societies must mean an unlimited number of small ones, never Societies of unlimited size. The charter forbids merger into national bodies, caps each Society at the point where the manager still knows the residents' names, and bars the subsidiary trick outright. Plurality and smallness are the protection. Scale is the solvent which dissolves it.

A Society also need not be a single built village, and forcing such a form on the whole country would strand the people least able to move. The model bends to its setting.

- In the countryside it can be dispersed: a rural Society which knits together members living in their own homes across a market town and its villages, with a shared hub for meals, care coordination, clinics and company, and care brought to the cottage rather than the cottage abandoned for an institution.

- In a city it need not be a village at all, but a converted civic block, a courtyard development, or a cluster of streets gathered around a dining hall and a clinic, dense and woven into the life of an existing neighbourhood rather than set apart from it.

The "village" is a shorthand, not a requirement; what matters is the membership, the ownership, the care and the protections, not whether there are hedgerows.

The same body, the same vesting and the same locks serve a widow on a Dales farm, a retired docker in a terrace street, and a Bengali grandmother in an East London courtyard alike. The Society comes to where people already are, urban or rural, rather than demanding they uproot to reach it.

Smallness carries a second gift: particularity.

A Society can be shaped around a place, a faith, a trade or a shared life, rather than flattened into a national template. A mining-village Society, a Catholic Society, a Society of retired seafarers, a market-town Society, each reflecting the people who built it. The state guarantees the person and sets the floor. It does not impose a uniform, because a uniform is the enemy of the belonging that makes the whole thing work.

Particularity must not curdle into segregation by wealth, though, or the whole moral claim of the same front door is lost and the framework becomes a chain of gated enclaves for the well-organised rich.

The guard against this is a condition rather than an exhortation. The advantages a Society enjoys, its tax-free status, its access to public land, the public guarantee standing behind its dependency cover, are granted only on terms:

- Every Society must hold a mixed membership and accept a minimum share of floor-supported members.

- A Society which wants to be a luxury retirement village for cash buyers is free to try, but it forfeits the land, the tax shelter and the guarantee, which is to say it is no longer a Commonwealth Society at all. The public support buys public obligation.

This does not mean every room is identical or every comfort is free, which would be a fantasy no Society could fund. A member who paid in more may have a larger flat or buy extras a poorer member does not.

What the rule guarantees is the part that matters: the floor-supported member comes through the same front door, eats in the same dining room, joins the same community, and gets the same standard of care as anyone else.

Different curtains, the same dignity. The poor age in the same place because the rich cannot have the place without them.

Seven Protections Against Capture

Every institution built for the public good is eventually circled by people who would like to own it, hollow it out, or run it from a ministry. The two nightmares for this framework are obvious: that it becomes Whitehall with gardens, a nationalised care estate run for the convenience of the state, or private equity with a chapel, a mutilated mutual sector stripped for yield.

Seven hard rules, written into the charter and enforceable in court, stand against both.

- First, no state operation. The state finances, guarantees and sets the floor, and never runs a Society.

- Second, no outside equity. No investor can take a stake, because there is no stake to take.

- Third, no demutualisation. The asset lock is permanent and cannot be voted away by a board that has spotted the value inside.

- Fourth, no national consolidation. Societies cannot merge into giants; the network grows by multiplying small bodies, never by enlarging them.

- Fifth, no for-profit subsidiaries capable of extracting surplus or holding the core assets, the device through which asset locks are quietly bent elsewhere. A Society may own a tightly limited service arm, a café, a maintenance company, a shared purchasing body, but it must be wholly owned, barred from holding the homes or the land, and barred from paying profit out beyond the lock.

- Sixth, portable member rights and a real exit, so that no Society can trap the people it serves.

- Seventh, a court-enforced asset lock and the guardianship protections, so that the walls are defended by judges rather than by the goodwill of whoever happens to sit on the board.

If a Society becomes insolvent, the asset lock survives the insolvency. Homes, land and member records transfer to another Society, a temporary administrator, or a successor body under tribunal supervision. Members do not become unsecured creditors of their own old age.

None of these is decorative. Each closes a specific door through which the mutual sector was looted the first time, or through which the state absorbs everything it touches.

Together they are the reason a Commonwealth Society can be trusted to still be a Commonwealth Society in fifty years, rather than a brass plaque on something which has become its opposite.

Money Building Something On Its Way Through

The state pension is pure consumption. The money arrives, it is spent on subsistence, and it leaves no trace beyond the survival of the recipient for another week. Hundreds of billions a year flow through the system and build nothing, own nothing and compound into nothing.

This is the hidden waste of pay-as-you-go: it is not merely fragile, it is barren.

A Commonwealth Society puts the same broad flows of money to work twice, once as care and once as capital, and leaves a country richer in buildings, jobs and owned assets than it found.

A national network of Societies is, among other things, the largest programme of beautiful, human-scale building Britain has attempted in generations.

Every Society is a commission: housing, dining halls, workshops, gardens, clinics, built to a statutory standard of beauty and, wherever possible, from local materials by local trades. That is sustained demand for architects, masons, joiners, gardeners and small builders, spread across every town rather than concentrated in a few cities, and aimed at structures meant to last a century rather than the disposable boxes the present care sector throws up.

The capital accounts themselves, pooled into low-cost national funds, become a vast domestic pool of patient investment, the kind of long-horizon capital Britain chronically lacks, available to fund the very construction the Societies require.

Each Society is a permanent local employer of carers, cooks, nurses, gardeners, drivers and managers, jobs rooted in a specific community that cannot be offshored and do not vanish in a downturn, because old age does not pause for the business cycle. These are exactly the productive, dignified, local jobs that hollowed-out towns have lost, created not by subsidy but by the ordinary operation of an institution the community owns.

And because the Society is asset-locked and member-owned, the surplus it generates cannot be extracted to a private-equity fund in another jurisdiction. It stays, reinvested in the place, in better buildings and higher wages and lower fees, compounding locally rather than leaking away.

The elderly themselves stop being treated as pure cost and become, in part, capital. A Society is full of people with trades, knowledge and time: retired engineers who can teach apprentices, former teachers who can tutor, gardeners, cooks, carers, mentors. Service counts toward standing precisely because that labour is real and valuable, and a Society that draws on it runs cheaper and richer than a warehouse that treats its residents as inert.

The wisdom and the working hours of the old, written off entirely by a system which simply pays them to wait, are put back to use.

The state pension imports workers to sustain consumption and builds nothing with the money.

This framework builds the places, employs the people, keeps the surplus local and turns the elderly back into contributors.

One settlement treats an ageing population as a bill to be paid and a demographic hole to be backfilled with migration. The other treats it as the occasion for the largest civic construction and the deepest pool of patient capital the country has seen in a lifetime.

The Boundary With Healthcare

A Society which runs a clinic and a nursing floor becomes a care provider, and the line between it and the universal healthcare framework has to be drawn cleanly, or costs leak across it in both directions. The clean line is acuity.

More on the Universal Health Framework here:

The Society handles primary, chronic, frailty, rehabilitation and palliative care inside its own walls, where nearness and a long-known history matter most. The acute universal system handles surgery, emergencies and complex diagnostics.

The incentive between the two has to be drawn with care, or it becomes a reason to keep a sick member away from hospital. The line is precise:

- Clinically necessary acute care is always fully covered by the universal system and never counts against the Society, while -

- Preventable admissions and the costs of delayed discharge, the member left on a ward because no one arranged their return, are charged to the Society's dependency budget.

A Society is penalised for the hospital stays its own neglect caused, never for the ones a member genuinely needed.

That distinction is what makes on-site care reduce the national bill rather than relocate it, and it points every Society toward the prevention and early intervention the present fragmented system has no reason to bother with, without ever giving it a motive to withhold real treatment.

An Accrued Promise Ledger: Honouring Old Promises Honestly

The genuinely hard part is transition, because millions hold a legitimate expectation built across a working lifetime, and any honest scheme must honour it without pretending the bankrupt machine can keep issuing fresh promises.

The governing principle is easy to state and hard to execute: promises already made are honoured as far as they can be, but no new promises are issued under a model that cannot pay.

In practice that means a staged settlement by age.

| Cohort | Treatment under transition |

|---|---|

| Current pensioners | Fully protected. Nothing changes. |

| Within 10 years of retirement | Largely protected, with top-end means-testing. |

| 10–25 years out | Hybrid: accrued state-pension expectation converted into a retirement credit. |

| Under 40 | Primarily moved to the Personal Capital Account, with a head start to compensate. |

| New entrants | No old-style entitlement; they begin inside the new system. |

The instrument which makes this acceptable is the Accrued Promise Ledger. Every citizen receives a single honest statement showing what the old system notionally owed them, what portion is protected, what portion converts into their own Personal Capital Account, and what the rules are from this day forward.

People will accept enormous change when they can see the swap laid out plainly. They will not accept a confiscation conducted in silence, and they are right not to.

The cost of the transition is real and should not be disguised.

For a generation, the working population funds both the protected promises of the old system and their own accounts under the new one, the double-payment hump every shift from pay-as-you-go to funded provision must climb. No ownership structure makes that hump vanish, and a serious proposal has to name where the money comes from rather than waving at "savings". The sources are specific.

- National Insurance is redirected in phases rather than abolished overnight, so the old promises stay funded while new contributions begin to accumulate.

- The triple lock ends, and the affluent-pensioner add-ons are means-tested, releasing money immediately.

- A temporary, time-limited transition levy carries part of the load, paired with long-duration transition bonds which spread the hump across the generations who will benefit from it rather than dumping it on one.

- Surplus public land and assets are transferred into the Society network rather than sold for cash that vanishes into a single year's budget. Planning uplift is captured where land is converted.

- Housing equity flows in through the estate-backed charge, and private pension transfers bring existing capital into the system.

And against all of this sits a genuine saving: a population ageing inside well-run Societies, kept well at home and out of hospital, reduces the future bill for acute healthcare and emergency social care the present system pays again and again.

The generation climbing the hump is not merely taxed to honour a fiction. It is building the institutions, the buildings and the capital its own children will inherit.

Because those sources arrive at different times, land and housing equity and hospital savings do not pay next year's pension bill, the transition runs in three plain stages rather than all at once.

| Stage | What it does | Chief instruments |

|---|---|---|

| One: stop the bleeding | End the growth of the unfunded promise | No new old-style entitlements, triple lock abolished, future promises frozen and converted |

| Two: fund the hump | Carry the double-payment years | Phased NI split, time-limited transition levy, long-duration transition bonds, public land and asset endowment |

| Three: run down the old promise | Honour what was promised as it expires | Current pensioners protected, near-retirees honoured, younger cohorts fully shifted to the new system |

Stage one costs almost nothing and starts immediately, because stopping a liability from growing is the cheapest thing a government ever does.

Stage two is where the borrowing and the levy do their work, smoothing the peak across the bondholders and the generations who will benefit rather than dropping it on a single cohort.

Stage three simply lets the old system age out: the protected promises are paid until the last person owed them has died, by which time the new system has long since taken the weight.

The lumpy, slow-arriving money, the land, the uplift, the equity, the health savings, accrues across stages two and three, paying down the bonds rather than being expected to cover a bill the year it is needed.

Several things are abolished outright, and should be named without euphemism:

- the triple lock,

- the National Insurance contributory fiction,

- the universal state-pension entitlement for future cohorts,

- Pension Credit as a separate maze,

- the politicised winter fuel payment, and

- the single magical cliff-edge of a fixed pension age.

Retirement becomes a band, perhaps sixty to seventy-five, with actuarially adjusted access, rather than a date on which the state abruptly owes you money.

And the band bends to the body. The framework distinguishes the end of physical labour from a chronological age, because a roofer and a registrar do not wear out on the same schedule.

Demonstrable physical incapacity opens earlier access; retraining credits, lighter-work pathways and trade-teaching roles let those whose bodies have given out move to work they can still do rather than be discarded; and service-credit routes give the low earner who cannot simply save more a way to build standing through their hands.

A settlement which ignored this would be just another rule written by people whose work never touched their joints.

What This Is Not

The proposal is unusual enough that readers will reach for a familiar box to put it in, so it is worth saying plainly which boxes are wrong.

- It is not a national chain of care homes run from Whitehall. The state finances and guarantees but never operates a single Society.

- It is not a private pension with bunting on it; the account is only the plumbing, and the place is the point.

- It is not a subsidised luxury village for the comfortable, because the tax relief and the land come with a binding duty to take the poor through the same door.

- It is not a state commune; a Society is owned by its members, plural and particular, free to be Catholic or secular, urban or rural, a miners' society or a seafarers' one.

- It is not a house grab; the charge on a home is optional, capped, advised, and never the price of belonging.

- It is not a regulator's empire; the enforcement lives in members' rights, families, courts and a single narrow inspector, not a new quango.

- And it is not uniform provision handed down from the centre; the floor is universal, but the institutions are many and made by the people in them.

Stated positively, in one line: it is a protected legal form through which ordinary people can turn money, land, service and time into a known and dignified later life. That is all it is, and there is nothing else quite like it on offer.

Fear That Lifts Decades Before The Crisis

Return to the woman of forty. Under the old settlement her future is fog. She works, pays her tax, and hopes the state still has money when she arrives, hopes her family can cope, hopes the care home is not a horror, hopes her children can untangle the probate once she is gone. Hope is doing all the work in that sentence, and none of it is hers to control.

Under the Commonwealth Society framework she joins a Society, contributes through wages and service across the years, and watches a place take shape that she has helped build and will one day belong to. If her husband dies, there is a dining room and a community and people who will notice. If she declines, there is care that already knows her. When she dies, the house and the funeral and the papers are handled, and her children inherit clarity rather than chaos, very possibly with capital attached.

The fear does not vanish, because nothing makes mortality painless, but it loosens its grip decades early, because the ending is no longer a void.

That is the real inversion of the moral argument.

The defenders of the state pension have spent decades accusing reformers of cruelty while administering a system which hands the old just enough money to be alone.

The cruelty was never in proposing to replace it. The cruelty is in pretending a weekly payment was ever enough. The state pension is not too generous. It is too small a vision of what a human life is owed at its close.

Britain built the mutual sector once, out of nothing but the conviction people facing the same fate should face it together, then let the state hollow it out and the market pick the bones. The Commonwealth Society is not an invention. It is a recovery, aimed at the one corner of life where being known turns out to matter more than being paid.